Overview

- The House Ways & Means1 Committee released its draft language for the ‘Big Beautiful Bill,’ which includes a number of components impacting nonprofit organizations. The components impacting investment pools are related to new or additional taxes.

- The Endowment Tax proposal aims to expand eligibility and how much those eligible pay. It includes a tiered rate structure based on asset-per-student amounts, and the inclusion criteria would narrow which students can be included in the calculation, for example excluding international students on temporary student visas.

- The Private Foundation Tax proposal mirrors the Endowment Tax proposal, moving from the current single 1.39% rate to a tiered rate determined by asset levels. Importantly, the tiers are determined by a foundation’s total assets, not just investment assets.

- The Joint Committee on Taxation estimates these two initiatives will raise $22.6B over the next 10 years.

- If passed, these new taxes will pressure higher education institutions and private foundations to reconsider their investment strategies and budgets.

- It is important to remember in the United States, bills often undergo many changes before becoming legislation. The original 2017 House tax bill proposed a 1.4% excise tax for private institutions with at least 500 tuition-paying students and endowment assets exceeding $100,000 per full-time student.1 This would have affected approximately 140 to 155 institutions, instead of the 56 it did in 2023 when that $100,000 was increased to $500,000.2

Endowment Tax Refined

This refined proposal expands who is subject to the endowment tax and creates a wider range for the amount of the tax.

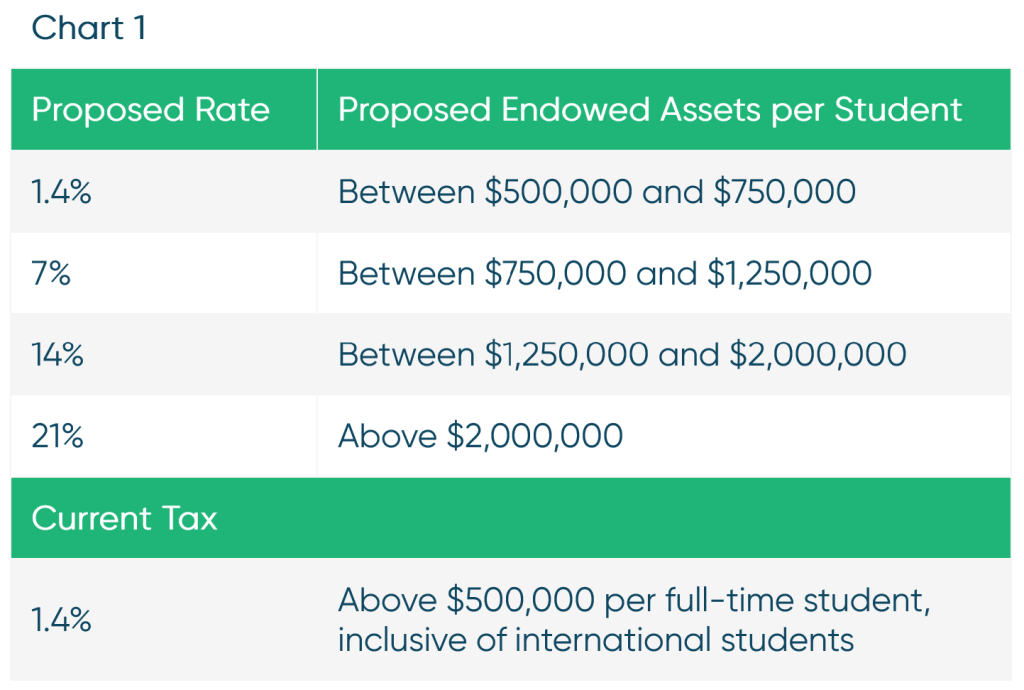

- Rate: Increases from a single 1.4% rate to a tiered system with the highest rate set at 21%. An endowment will pay a single rate on all net investment income.

- Tier Determination: Endowed assets per student will determine what tier of tax an endowment will pay. See Chart 1 below for the tiers and rates.

- Student Count for Tier Calculation: Narrows the students that can be included, specifically excluding international students.3

While everyone anticipated a higher tax rate, they were not anticipating the exclusion of international students. This exclusion favors US citizens, permanent residents, or those not here on a temporary basis. It disproportionately and negatively impacts institutions with large international populations, such as those with graduate programs, which tend to have a larger percentage of international students.

We have already written about the three original proposals in February/March 2025 when they were released. Please refer to The Impact of Proposed Endowment Tax Changes and Endowment Tax – Part 2: Impact on the Endowment.

The Joint Committee on Taxation estimates this will generate $6.69 billion over 10 years.4

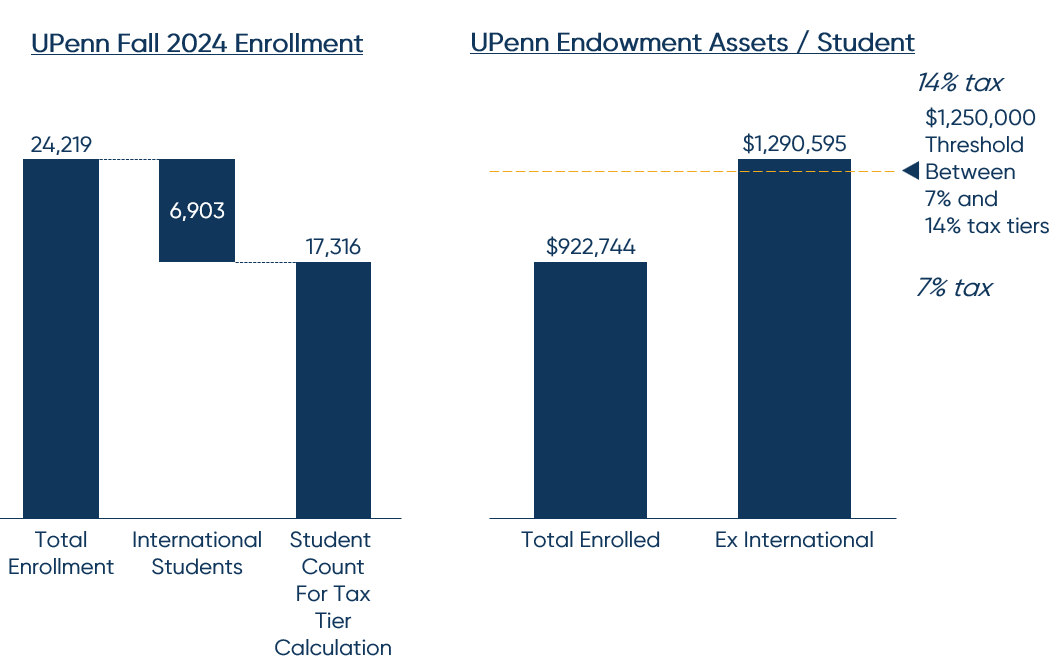

Case Study: International Exclusion May Push UPenn into 14% Tier

The exclusion of international students in the student count for tier determination is important. The University of Pennsylvania had 29% international students enrolled in Fall 2024. Utilizing the total number of enrolled (or even just full-time students), Penn would be in the 7% tax tier. However, with the international students excluded, Penn is now in the 14% tax tier–double the tax of the lower tier it would have previously qualified for if its full student population was counted, and 10 times its current tax of 1.4%.

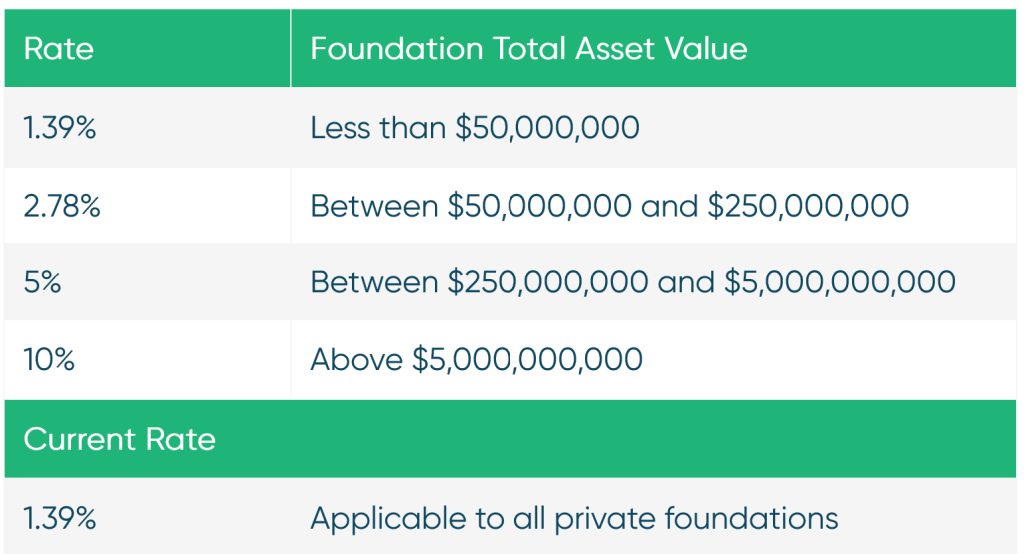

Private Foundation Tax to be Tiered

This proposal increases the amount of tax certain foundations will pay in the future. Today all foundations pay a 1.39% tax.

- Rate: Increases the 1.39% single-tier tax to four rate tiers with the highest rate set at 10%. A foundation will pay a single rate, based on its tier, on all net investment income.5

- Tier Determination: the total foundation’s assets will determine what tier of tax an endowment will pay, not just investment assets. Total foundation assets include all assets, with no reduction for liabilities, and would also take into account assets of certain related organizations.

The Joint Committee on Taxation estimates this will generate $15.88 billion over 10 years.6

Summary

For institutions, a new or increased tax, depending on the tier, has varying level of impact–from small (1.4%/1.39%) to significant (21% for endowments or 10% for foundations). Impacted institutions may need to consider how the reduction in invested assets, and thus reduced spending, may necessitate changes to the budget or investment pool. TIFF has discussed the potential impact and implications of the endowment tax previously, summary of which is:

- Budget Implications: Institutions may need to reconsider their budget if suitable long-term replacements are not feasible for lost budgetary support from the investment pool.

- Investment Implications: If an institution is in a high enough tax tier, it may need to consider changing its approach, potentially increasing its risk tolerance or shifting asset allocation to incur less investment income.

These proposed changes and the associated implications create a challenging time for the nonprofit community. TIFF remains committed to helping organizations determine the right investment strategy for their unique situation.

The materials are being provided for informational purposes only and constitute neither an offer to sell nor a solicitation of an offer to buy securities. These materials also do not constitute an offer or advertisement of TIFF’s investment advisory services or investment, legal or tax advice. Opinions expressed herein are those of TIFF and are not a recommendation to buy or sell any securities.

These materials may contain forward-looking statements relating to future events. In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expect,” “plan,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” or “continue,” the negative of such terms or other comparable terminology. Although TIFF believes the expectations reflected in the forward-looking statements are reasonable, future results cannot be guaranteed.