Executive Summary

- Our last article focused on endowment tax proposals and how they may impact educational institutions directly.

- This article looks at the specific impact on the endowment portfolio.

- Today’s 1.4% tax is expected to cause a reduction of 5-15 basis points in net returns, according to TIFF estimates. A tax increase to 10% or above starts to be meaningful.

- This tax introduces an issue where institutions may no longer be able to maintain inflation-adjusted purchasing power after spending and tax with their current target returns.

- If a 10%+ rate is enacted, institutions will face a delicate balance between reconsidering asset allocation to reduce tax burden, potentially increasing risk to increase expected return, or decrease spending.

- TIFF will continue focus on the topic as new information becomes available.

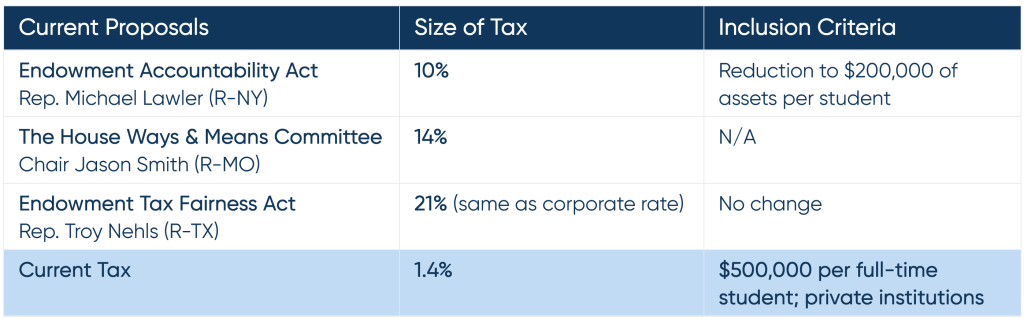

As a Reminder: Summary of Proposals

In our last article, TIFF outlined the various endowment tax proposals. Below is a summary:

Endowment Tax Impact on Portfolio Returns

It is important to remember this tax is levied on net investment income, not total assets, so any headline tax rate is diluted. “Net investment income” includes everything from capital gains to dividends (investment income passively obtained), net of eligible deductions such as advisory and brokerage fees.[i], [ii] This tax is charged on realized gains/income, meaning that even in a negative performance year, the endowment could incur a tax liability.

TIFF has estimated the impact of the current tax (1.4%) and various proposals on after-tax net returns for endowment style portfolios.[iii]

- The current tax has minimal impact on after-tax net returns; TIFF estimates this causes a reduction of 5-15 basis points of net returns.

- A tax increase to 10% or above starts to be meaningful.

- TIFF has added a “plausible compromise” scenario of a 5% tax, which is noticeable, though not dramatic, at an estimated 20-40 basis points drag per year.

Estimated Excise Tax Impact on Net Returns

Potential Implications for the Endowment

At a 1.4% tax, institutions are unlikely to adjust their portfolios. However, a tax rate of 10% or higher would likely prompt institutions to explore options to manage the tax impact. There is no single solution to the endowment tax. Addressing the implications of the endowment tax will require a multi-dimensional approach, balancing reconsidering the spend rate, increasing the expected return slightly, and tweaking the investment strategy to reduce the annual tax burden–all while trying to maintain support for the institution and best practices of portfolio construction.

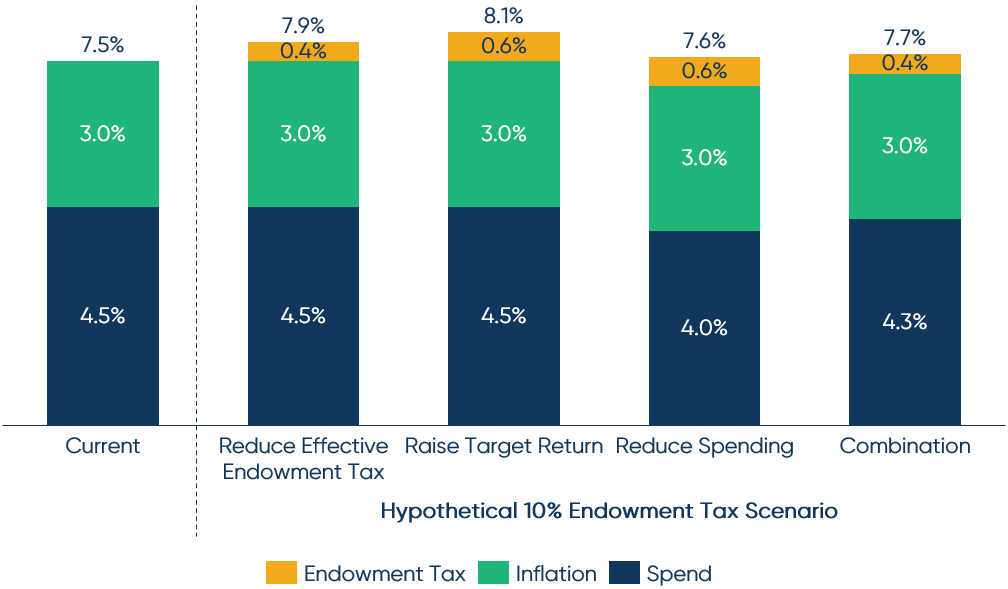

This tax introduces an issue where institutions may no longer be able to maintain inflation-adjusted purchasing power after spending and tax, with their current target returns. The graph below shows an illustrative scenario for a hypothetical educational institution with a 4.5% spend rate. Without tax, their target return is likely around 7.5%. However, the introduction of an endowment tax reduces the net returns available for compounding. TIFF has outlined three potential solutions institutions may look at individually, or in concert, to address this issue.

Hypothetical Target Return Requirement Build-up

- Reduce tax burden by revising asset allocation: Tax is on net investment income, which mean it taxes all realized gains in a year equally. Altering the types of investments the endowment is invested in may help to reduce the tax burden. Two broad approaches are:

- Increase allocation to assets that defer realizations (e.g., long-hold equities, private equity).

- Decrease allocation to assets that have high annual income/gains (e.g., fixed income, high-turnover hedge funds, income-focused core real estate).

- Increase target return via increased risk level to (partially) offset the tax: With no change in spend, a tax will increase one’s target return requirements (CPI+spend rate+annual tax rate). However, a balance must be struck between increasing the target return, and therefore overall risk, and decrease in spend rate. This may not be feasible for many institutions who already are at their risk tolerance.

- Non-Endowment Option: Decrease the spend to offset the tax: While a difficult conversation depending on how large the tax is, discussing the spend rate and likelihood of hitting an institution’s long-term inflation-adjusted real rates of return post-spend will be important.

Conclusion

This topic is still emerging with various proposals at play. TIFF remains engaged and focused on the topic, helping our clients understand the implications. If your institution believes it might be at risk for inclusion, please reach out to your TIFF team for further discussion.

The materials are being provided for informational purposes only and constitute neither an offer to sell nor a solicitation of an offer to buy securities. These materials also do not constitute an offer or advertisement of TIFF’s investment advisory services or investment, legal or tax advice. Opinions expressed herein are those of TIFF and are not a recommendation to buy or sell any securities.

These materials may contain forward-looking statements relating to future events. In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expect,” “plan,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” or “continue,” the negative of such terms or other comparable terminology. Although TIFF believes the expectations reflected in the forward-looking statements are reasonable, future results cannot be guaranteed.

[i] https://www.irs.gov/newsroom/irs-issues-guidance-on-the-tax-on-the-net-investment-income-of-certain-private-colleges-and-universities

[ii] https://www.irs.gov/newsroom/questions-and-answers-on-the-net-investment-income-tax

[iii] Endowment style portfolios are defined as portfolios with high allocations to alternatives, including hedge funds, private equity and venture capital.