Introduction

The recent actions taken by the Trump Administration against Harvard University have sent shockwaves through the higher education community. With investigations into Antisemitic discrimination, demands for sweeping reforms, and threats to revoke tax-exempt status, the federal government is challenging the autonomy and operational frameworks of one of the nation’s most prestigious institutions. This brief article explores the unfolding situation, the positions of both Harvard and the federal government, and the broader implications for non-profit universities across the United States.

What is happening with Harvard and the Trump Administration

- The Department of Education (DOE) sent 60 universities notice that they were under investigation for Antisemitic discrimination and harassment.1 It was noted federal funding would be revoked for those that don’t accept required steps to protect Jewish students.2 Columbia University was the first target, which currently negotiating with the federal government after $400M of funding was frozen.3

- The Department of Education sent Harvard a list of refined requirements on April 11, which included eliminating diversity and inclusion programs and enacting merit-based hiring and admission reforms, banning masks on campus, and reducing power of faculty and administrators.4

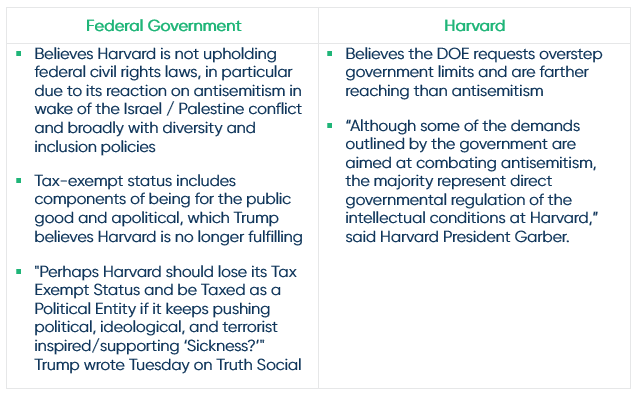

- Harvard responded on April 14 that it will not comply with the request, arguing that the changes requested by the government exceed its lawful authority and infringe on both the University’s independence and its constitutional rights.5 6

- The Federal government has retaliated by blocking $2.2B in funding slated for Harvard.

- The IRS investigation into revoking Harvard’s tax-exempt status7 and the Department of Homeland Security review of Harvard’s ability to enroll foreign students were announced this week.8

- Non-profits face significant risks including a potential larger role of government at U.S. universities, potential loss of tax-exempt status, the financial impacts of losing Federal funding or revenue tied to foreign student enrollment, and becoming a tax-paying entities.

The Two Sides

What is at Stake

The outcome, if in the Federal government’s favor, will change the rules of engagement for U.S. education and have long lasting impacts on U.S. higher education on the involvement and control.

Precedent for Loss of Tax-Exempt Status: This would set a precedent for U.S. higher education losing tax-exempt status if they do not align with views of being apolitical and for the public good. One would imagine those definitions are qualitative at times and any potential loss of status will be left to the courts.

Loss of Tax-Exempt Status Financial Impact: Harvard would become a for-profit entity, meaning the entire institution would now be subject to taxation. This would be broader taxation than its current endowment tax, which is restricted to endowment net investment income. Corporate taxes are charged at the entity level. In addition, Harvard would now be subject to state and local taxes.

Bloomberg estimated Harvard’s property taxes alone at $465M, with assessed property at $4 billion in Boston and $8.7 billion in Cambridge.9

Where are those taxes coming from?

- Federal Corporate Rate: 21% on corporate profit

- State Corporate Rate (MA): 8% on corporate profit

- Local (Boston, Cambridge): As one of the largest land-owners in the area, Harvard would now be subject to property tax in Cambridge and Allston. For example, Cambridge charges corporations $11.52 per $1,000 of assessed property value.10

Other impacts would be donations are no longer tax-deductible, likely leading to a decline in funding through donations.

All of these would require a structural change in how Harvard is structured and thinks about its financials.

Conclusion

The conflict between Harvard and the Trump Administration highlights the risks nonprofit universities face from increased government influence. If the government wins, it could set a precedent affecting tax-exempt status, funding, and institutional independence. Nonprofits should stay informed and be prepared for changes in regulations and resulting impact on finances. The outcome could impact not only Harvard but also the broader higher education sector, requiring a reassessment of the balance between educational autonomy and government oversight.

The materials are being provided for informational purposes only and constitute neither an offer to sell nor a solicitation of an offer to buy securities. These materials also do not constitute an offer or advertisement of TIFF’s investment advisory services or investment, legal or tax advice. Opinions expressed herein are those of TIFF and are not a recommendation to buy or sell any securities.

These materials may contain forward-looking statements relating to future events. In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expect,” “plan,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” or “continue,” the negative of such terms or other comparable terminology. Although TIFF believes the expectations reflected in the forward-looking statements are reasonable, future results cannot be guaranteed.

Footnotes

https://www.theguardian.com/us-news/2025/mar/21/columbia-university-funding-trump-demands

https://www.harvard.edu/president/news/2025/the-promise-of-american-higher-education/

https://www.harvard.edu/research-funding/wp-content/uploads/sites/16/2025/04/Harvard-Response-2025-04-14.pdf

https://www.cnn.com/2025/04/16/politics/irs-harvard-tax-exempt-status/index.html

https://www.cambridgema.gov/departments/finance/propertytaxinformation