Executive Summary

- Swift changes implemented by the Trump administration have led to increased market volatility and uncertainty.

- Recent tariffs imposed by the US on Canada, Mexico, and China have created significant economic uncertainty and negatively affected markets as we approach the April 2nd reciprocal tariff announcements.

- Economic indicators have weakened, with GDP growth expected to slow down and inflation predicted to rise, suggesting a challenging economic period may lie ahead.

- The administration’s focus on deregulation, including a regulatory freeze and efforts to rescind existing regulations, is expected to lead to legal challenges and further market unpredictability.

- Despite all this uncertainty we highlight the importance of maintaining a long-term investment focus amidst short-term volatility and avoiding hasty decision-making; stay focused on your investment goals.

- With that in mind, we are maintaining our strategic asset allocation with 65% in the All Country World Index (ACWI), 20% in hedge funds, and 15% in the Bloomberg Aggregate Bond Index (AGG).

Fast and Furious

In previous letters, we’ve mentioned a quote attributed to Vladimir Lenin:

“Sometimes nothing happens for decades, and sometimes decades happen in a week.”

We were referring to the rapid impact of AI on our world. Since Donald Trump’s re-election and return to the White House, events seem to be accelerating faster than ever.

Every new president promises change, but none has delivered as swiftly as Trump has in his second term. It is worth noting that he signed 26 executive orders on his first day back in office and has reached 92 as of March 20, 2025, in addition to the 220 he signed during his first term. For comparison, Biden signed 160 executive orders in four years, Obama 276 in eight years, and Franklin Roosevelt holds the record with 3,721 over 12 years. Keeping up with these changes has been challenging and exhausting for most.

There is significant debate among intelligent and honest people about the effectiveness and potential outcomes of most of Trump’s ideas. As new ideas emerge and are debated, they naturally create more questions and uncertainty. We anticipated significant change under Trump, but the pace of change has been dizzying even for us.

Let the Chaos Begin

On March 4, 2025, Trump’s first tariffs on Canada and Mexico took effect, along with an additional 10% tariff on China. The reasons given for these tariffs were sometimes economic and sometimes to punish a country for allowing fentanyl and other harmful agents to come into our country. Canada and China retaliated, and Mexico was expected to announce retaliatory tariffs. Markets are reacting negatively. Many were surprised that Trump went through with the tariffs on Canada and Mexico, who seemed to be calling his bluff. Similarly, the February 28 Zelensky conflict at the White House cast doubt on the Ukraine/Russia peace process, as Trump temporarily halted US aid to Ukraine and upset our European allies. A few weeks later, most of these tariffs have been changed (and will be again on April 2), and Zelensky and Trump seem to be back on the same team, depending on the day. The apparent chaos of recent weeks is causing concern both domestically and globally and has increased market volatility. This is likely to continue as tariffs increase and negotiations everywhere on everything continue.

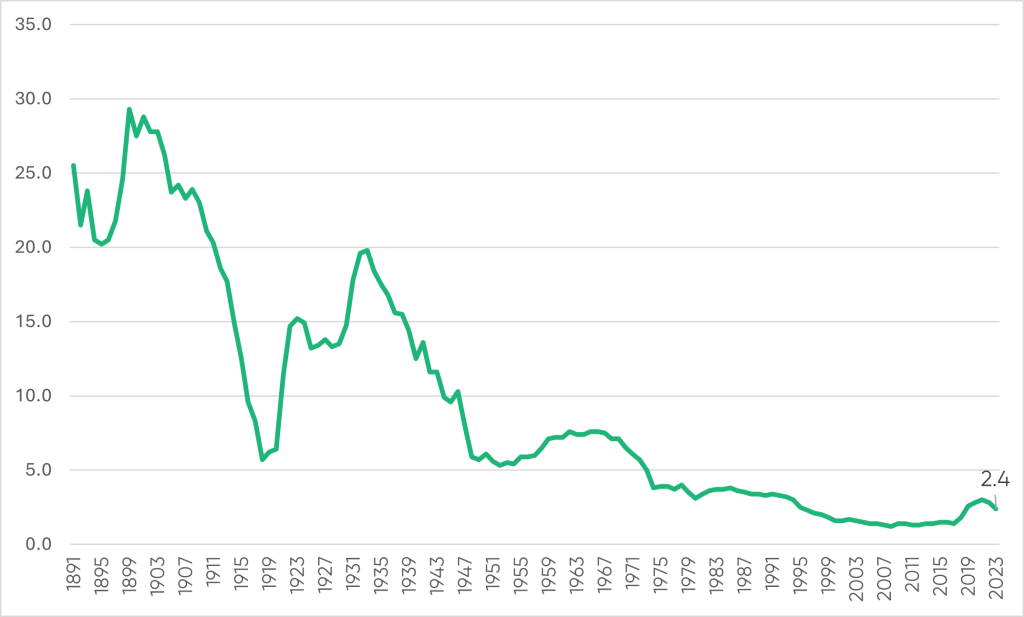

While Tariffs are Still Below Historical Levels, They are Reaching the Highest Levels Seen in Nearly 30 years

US Duties Collected as a % of Total Imports

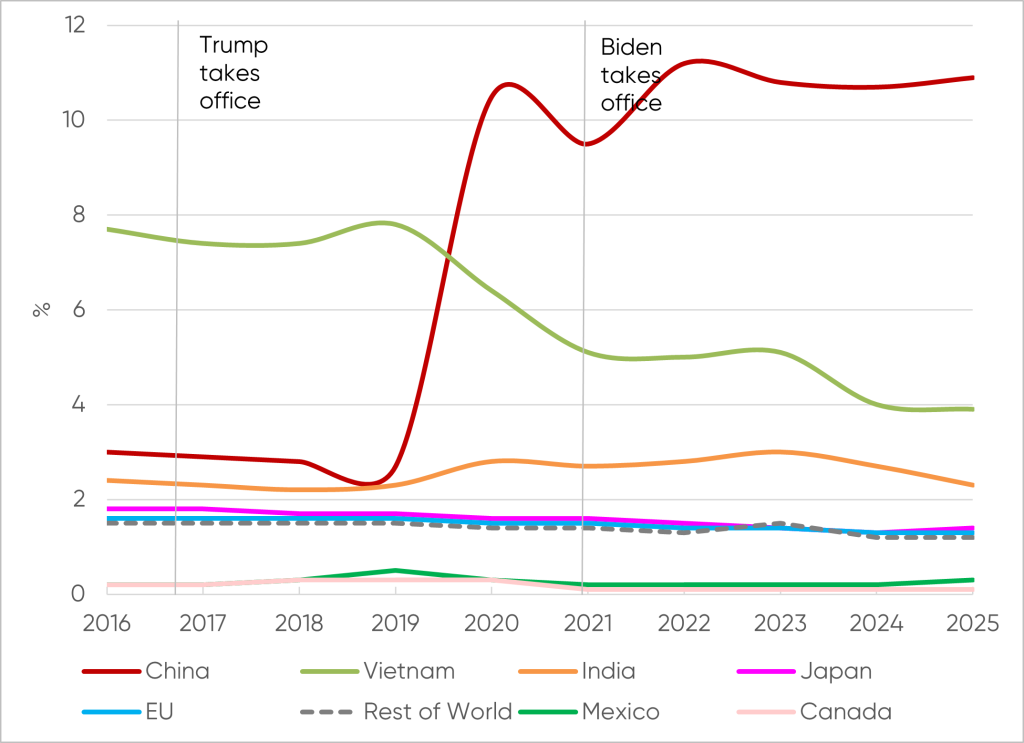

With the Exception of China, the US Tariffs on the Rest of the World are Still Rather Low, Meaning If the Trump Administration is Serious About Increasing Tariffs, We May Have a Long Way to Go

US Effective Tariff Rate by Import Source Country, 12-month Rolling Average

The most important tariff day looks to be April 2, when the US government plans to announce reciprocal tariffs. As we understand this undertaking, whatever tariff (including, in some cases, V.A.T) a country charges us is the tariff we will levy back on them. Ironically, this could either result in tariff wars or in a free trade relationship, depending on what tariff a foreign country chooses to charge us. The cone of possible outcomes around this is wide, increasing uncertainty. Several economic indicators have recently weakened, compounding the impact of this uncertainty and suggesting a challenging period may lie ahead for the economy and markets. The Federal Open Market Committee recently revised expected 2025 GDP growth down by 0.4% to 1.7% and inflation (core PCE) up by 0.3% to 2.8%. They expect tariff inflation to be “transitory” and left rates unchanged, noting that uncertainty has increased.

The new administration also is focused on removing regulations. In addition to implementing a regulatory freeze pending review and halting all new regulations, they aim to keep the total incremental cost of all new regulations in fiscal year 2025 to “significantly less than zero.” Agencies are directed to identify and rescind regulations inconsistent with Trump administration policies, and for every new regulation proposed, 10 must be identified for repeal. This leads to many de-regulation efforts being challenged in court, slowing their impact and likely sending some to the Supreme Court. It is a busy, unique, and chaotic time in Washington. The desired changes could lead to significantly better or worse outcomes, keeping markets on edge.

The Department of Government Efficiency (DOGE), which we hope can reduce the US government’s annual deficit by eliminating waste, fraud, and abuse within the Federal government, is off to a mixed start. While the website “polymarket.com/doge” suggests they have already identified $115 billion in annual savings, the media focus has been more on Elon Musk and the number of jobs potentially impacted. A respected research service recently increased their estimate of government worker layoffs before July 4, 2026, to more than 10% of current employees. This adds to current economic concerns and raises questions about the follow-on impacts, further exacerbating market uncertainty.

US stocks have accordingly fallen, dropping over 9% from peak year-to-date gains of nearly 5% to now sit near -4% for the year. Meanwhile, ten-year treasury bonds have rallied in price by about 3%, pushing the yield from 4.6% in January down to 4.2%, near the lowest since last September. This performance combination usually suggests a weakening economy and slowing earnings, ultimately pulling inflation down. Interestingly, while President Trump and his team believe targeted countries will pay the tariffs, most economists view tariffs as a tax that US businesses and consumers will pay through higher prices. Stocks could decline in either case, but if inflation rises rather than falls, the current decline in bond yields may be temporary.

S&P 500 Pulled Back to Pre-Election Level Following Strong Market Growth

S&P 500 Net Total Return (12/31/2023 – 03/31/2025)

A Word of Caution

Before we get into what we are doing about this elevated uncertainty, let us tell you what we aren’t doing: we aren’t getting swept up in the short-term day-to-day uncertainty. When investors start making major decisions based on short-term changes in macro numbers, we think that is risky. We’ve recently read that the most important decisions one needs to make today include whether the US is going to become partners with Russia, how the Middle East will end up, how much tariffs will increase inflation, how badly the DOGE layoffs will impact the economy, whether US exceptionalism is dead and US equities should be underweighted, etc. We don’t profess to know the answers to these questions. Yes, we have hunches and opinions like everyone else, but we also have enough experience to know that we don’t know nearly enough to correctly predict any of these outcomes let alone the preponderance of them.

Making too many decisions is usually harmful to long-term returns. I’ll briefly share my first lesson on this. On Black Monday, October 19, 1987, the Dow Jones fell by 22.6%, the largest one-day percentage return on record. Many people believed this signaled that the US was entering a depression ala 1929, the previous largest one-day percentage decline (-13.5%). As a 20-something-year-old, how could I disagree? I read all the “analysis” of the day, which was very lopsided, suggesting it was a fait accompli. My then CIO, Dick Huson, admitted that he didn’t know but strongly encouraged us to appreciate that nobody else did either, and so we should stay the course. He noted that the drop was many standard deviations above average, and it was a poor time to sell (it turned out to be a 28 standard deviation event, equivalent to a man who is 300 miles tall!). One month later, the S&P 500 returned 7%, and three months after that, it appreciated 18%. There was no depression; instead, we had elevated volatility and attractive returns.

Another event worth mentioning is the Global Financial Crisis of 2008, the biggest peak-to-trough loss since the great depression. The S&P peaked on October 11, 2007, before the US housing bubble-inspired credit crunch brought the financial world to its knees. As the world watched, the Fed let Lehman Brothers collapse, and financial contagion threatened further collapses. Markets fell precipitously before cooler heads finally prevailed, but not before the market had fallen nearly 57% by March 9, 2009. Four years later, the S&P had gained 150% (nearly 26% per annum) to recover to its previous high. Ten-year returns from the pre-crash high in 2007 were 104%, equal to 7.4% per annum.

Timing the exact moment to get out of and then back into the markets is very difficult. This is why we partner with some of the very best managers in the world and why we try to limit the number and size of decisions we make. The stock market can be volatile and can go down. Nevertheless, we have not found a liquid asset that can provide better, reasonably consistent, above-average long-term returns to hold in our portfolios. This is why we are careful not to get underweight equities and will only modestly overweight them if we believe a significant opportunity exists. When asked, we counsel others to do the same if they are trying to generate above-average long-term results.

Enough, what are we doing?

For now, we assume mainstream economists are correct in believing tariffs will negatively affect the US economy. Estimates are changing quickly, but aggregating estimates from different sources suggests that the US GDP is expected to slow down by 0.5% – 1% due to the expected newly implemented tariffs. This could lead to job losses of up to 200,000 on top of those laid off by DOGE, and consumer prices could rise by 1%. Combined with immigrant deportations and strict border control, this should reduce aggregate consumer spending. On the flip side, the current tariffs could raise $1.5 trillion over the next 10 years. A 10% universal tariff could raise $2 trillion, and a 20% universal tariff could raise $3.3 trillion over that period. However, these estimates do not account for potential retaliatory actions by other countries or the duration of the tariffs. Our economic future is murkier than it seemed three months ago.

Are we trimming our equity holdings, you ask? Not yet. Looking forward, we see continued productivity gains in the US and globally from the adoption and incorporation of AI within businesses. Some early adopters are experiencing radical productivity improvements, as noted in ARK Investments’ “Big Ideas 2025” report. They highlight how AI software engineering contributions have risen from 4% to 72% of work. In new drug development, the number of new hypotheses a research scientist could test in one year rose from 20 hypotheses tested in 2023 to 200 tested in 2024. ARK expects technological breakthroughs like these, and others in AI, Autonomous Mobility, and Humanoid Robots, to turbocharge economic growth over the next 5 to 10 years, potentially to as much as 7+% per annum. While this view is uncommonly bullish, AI is a very unique technology, and early adoption will accelerate productivity gains, living standards, and possibly markets.

One other area we are exploring is Europe. While the US is experiencing tremendous change, Europe is in the throes of generational change. We believe Europe’s newfound focus on self-reliance, more rational energy and fiscal policies, reduced austerity, less regulation, and more defense spending (much of these changes have been foisted upon them by a now undependable US) may allow Europe to emerge from what many perceive to be a self-induced 15- to 20- year malaise. The internal debate continues about whether Europe presents opportunities for additional investment in our portfolios.

Wrapping it Up

We have strayed further than intended in this letter. Our main point is that things are moving very fast. Volatility is likely to remain elevated for a time and will cause some investors to lose focus on their long-term goals and instead make unnecessary decisions that will likely need to be reversed. We try to avoid making too many decisions with poor information during these times and instead continue to look forward and stay focused on what the future world might look like. Skating to where the puck will be is always our goal.

Rather than make decisions under uncertainty, we believe now is a good time to look over the potential valley and ask ourselves how AI might impact the world in the next 3-5 years and what could that mean. We don’t know if markets will pull back as they did after the internet bubble or if the advancements this time are so significant that technology’s full valuation has not yet been realized. Combining an expected more volatile short-term period with a brighter long-term view, we will navigate this period by owning more hedges designed to capture market unease while partnering with the best managers globally and remaining invested for the long term. If the economy weakens and inflation decreases, bonds may perform better. Bonds could perform better still if the DOGE succeeds in cutting the budget deficit.

Equities are expected to experience increased volatility this year as the political environment seeks a new equilibrium and tariff uncertainties get answered. While tariffs may slow economic growth and boost inflation—potentially triggering stagflation fears—the expected productivity gains and growth benefits from AI adoption should help temper any excessive market pessimism. This period should be temporary. Subsequently, we can imagine a scenario where conflict fatigue leads to a calmer global environment. In this scenario, the potential success of the DOGE combined with lower taxes, less regulation, and more efficiency may allow the US to ease its tariff program, creating a more favorable cycle for both global GDP and equity markets. As we move forward, we will continue to share our thoughts and insights with you. For now, we are staying close to our strategic asset allocation targets: 65% in the All Country World Index (ACWI), 20% in hedge funds, and 15% in the Bloomberg Aggregate Bond Index (AGG).

As always, we greatly appreciate the opportunity to manage your capital and help you achieve your organization’s goals. We are here to assist in any way possible, so please feel free to reach out to us with any questions or needs.

Your TIFF Investment Team

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance. There is no guarantee that any particular asset allocation or mix of strategies will meet your investment objectives.

These materials are being provided for informational purposes only and constitute neither an offer to sell nor a solicitation of an offer to buy securities. These materials also do not constitute an offer or advertisement of TIFF’s investment advisory services or investment, legal or tax advice. Opinions expressed herein are those of TIFF and are not a recommendation to buy or sell any securities.

These materials may contain forward-looking statements relating to future events. In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expect,” “plan,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” or “continue,” the negative of such terms or other comparable terminology. Although TIFF believes the expectations reflected in the forward-looking statements are reasonable, future results cannot be guaranteed.